Ginnie Mae is a government corporation that is managing over $2.2 trillion of guaranteed Mortgage Backed Securities (MBS). We are, by our nature, managing a social good and balancing that with risk management practices that are designed to protect taxpayers and consumers from major economic events. Since announcing Ginnie Mae’s new independent mortgage bank (IMB) eligibility standard for applicants and approved issuers a month ago, we have been heavily engaged with the issuer community. We are adding clarity about how the standard operates and working with issuers to understand how they will use the next five quarters to come into compliance with our requirements. Our high touch issuer engagement approach informed the first set of FAQs we released last week, and we plan to continue to run a transparent and collaborative process. Our engagement with issuers will continue over the next several months and we are taking this opportunity to share some of the initial themes from discussions to date.

There has been a need for more clarity for the industry about the mechanics of the final Risk Based Capital Ratio (RBCR). To address this, we have included a simple example of the RBCR at the end of this Blogpost.

Underscoring the Crucial and Outsized Role of IMBs in the Government Mortgage Market

When we designed the new issuer eligibility requirements, our intent was to ensure they would not be disruptive. As of the second quarter of 2022, approximately 90% of roughly 200 Independent Mortgage Bank (IMB) issuers would be compliant with all new requirements, and 95% would be compliant with the RBCR.

We expect to see a large number of issuers continue their robust participation in the Ginnie Mae MBS program. We have heard from some industry observers that they are under the impression that only a small number of Ginnie Mae issuers hold servicing, with the remainder selling their MSRs to aggregators. As of the second quarter of 2022, over 70 IMBs held more than $1 billion of Ginnie Mae servicing and 32 of those each held more than $5 billion in servicing.

While some of those issuers that would not have been compliant with RBCR are large holders of Ginnie Mae servicing, it is important to recognize there are multiple ways to come into compliance, including raising additional equity capital and retaining earnings. All these measures add stability and strengthen issuers in the event of adverse market events or heightened liquidity and capital needs. If issuers determine that selling servicing is the optimal way for them to meet the risk-based requirements, they need only sell a portion of their servicing. And because Ginnie Mae’s risk-based capital requirement is agnostic with respect to which MSRs contribute to the total held, Ginnie Mae issuers could sell either Ginnie Mae MSRs or GSE MSRs to come into compliance. We are focused on mitigating any short-term market disruptions while issuers work through our requirements and their compliance plans over the next year. The year-plus implementation period will be critical to ensuring that potentially affected issuers have the time to plan and execute strategies for coming into compliance. Ginnie Mae’s engagement strategy is focused on understanding these plans in detail so that we can identify and mitigate issues before they significantly impact the market. For example, while we believe that five quarters is sufficient time to bring affected issuers into compliance, we need to understand their strategies so that we can ensure that compliance efforts do not cause dislocations in the MSR market.

The feedback we have received to-date has underscored that the opaqueness of the MSR market is a significant risk driver. Ginnie Mae cannot observe the MSR market directly and relies on ongoing discussions with issuers and third-party valuation agents for more depth on market trends. Lack of transparency in the MSR market adds to uncertainty about true value and may serve to increase price volatility. Another example of opaqueness in the market is the nature of sales or pledges of Excess Servicing Strips (ESS). While the sale of ESS is widely used, the nature of the risk transfer from buyer to seller varies based on each individually tailored contract. In some cases, providing full or partial capital relief to issuers that use ESS would be very reasonable. But given the highly variable nature of the ESS market, creating standard and transparent rule sets for capital relief would require corresponding minimum standards for ESS terms that would warrant capital relief.

Access to Credit for IMBs

One of our key objectives with the introduction of our new eligibility requirements is to ensure our issuers have reliable, long-term access to credit. While we do require that our issuers hold minimum levels of liquidity, it is unrealistic to expect that most can hold sufficient liquidity for their long term needs. As a result, IMBs must have reliable access to ongoing financing. In this sense, capital and liquidity are inextricably linked for IMBs. Our view, which we have confirmed with multiple creditors, is that our new eligibility requirements will increase market confidence in the ongoing viability of IMBs and will improve their access to lines of credit and liquidity resources.

This is why a robust capital standard is a critical component of Ginnie Mae’s approach to managing risk in the system. As President McCargo noted, the communities that depend most on Ginnie Mae issuers are the communities who stand to lose the most during an issuer failure or a broader housing downturn. By providing greater assurance that IMBs can access financing, we can ensure that IMBs can continue lending to new borrowers and helping homeowners in financial distress.

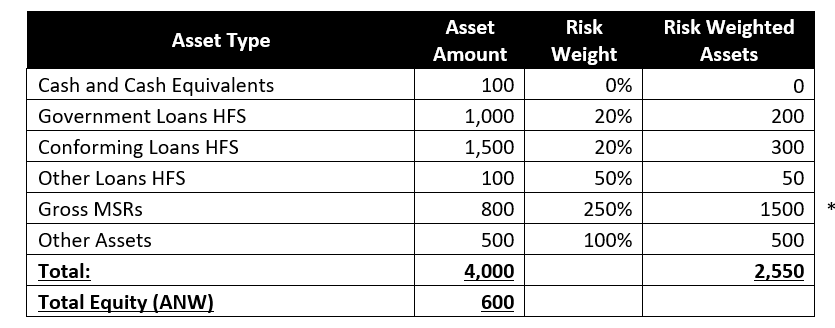

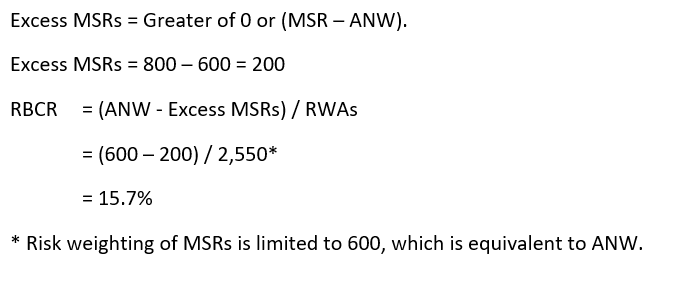

Risk Based Capital Ratio Example

Given the following Balance Sheet, including assets and ANW, we calculate the RBCR. We begin by calculating Risk Weighted Assets by applying the appropriate risk weighting to each category. When MSRs > ANW, we risk weight MSRs only in an amount up to ANW to avoid double counting the impact of MSRs in both the numerator and denominator.

Next, we deduct “Excess MSRs” from ANW. Excess MSRs are defined as the dollar value of MSRs that exceed ANW. In this calculation, the MSRs include all MSRs carried on balance sheet regardless of whether they are Ginnie, GSE or other servicing rights.

Sam Valverde is Executive Vice President and COO for Ginnie Mae

Greg Keith is Senior Vice President & Chief Risk Officer

Greg Young is Director of the Counterparty Risk Analysis Division